When it comes to personal income taxes, Singapore is among the countries in Asia that has the most favourable rates for individuals and businesses. It follows what is called a progressive income tax rate, a system which charges taxpayers with higher incomes a higher tax rate.

Even with the city-state having a maximum withholding tax rate of 20%, it still ranks pretty low among other countries. In Asia alone, it bests fellow neighbours like Japan, India, Korea, and the Philippines according to EY’s analysis of the 2015 budget.

Understanding the Basics

Personal Income Tax: The Terms for Residents

Generally, everyone who earns an income in Singapore is required to pay taxes. Individuals are taxed according to their residency—with residents being taxed under progressive terms and non-residents taxed a flat rate of 15%. Below is a more in-depth look at the terms for those considered as residents.

You are a tax resident if you:

1) Have spent at least 183 days in a year in the city-state. You are considered a resident of Singapore for that year and will be taxed progressive resident rates. You may claim tax reliefs.

2) Have spent at least 183 days in the city-state for a continuous period of over two years. You are considered a resident for the duration of your stay. Normal progressive rates and claim tax reliefs apply.

3) Have stayed in Singapore for three consecutive years. You are a resident during this time and will be charged progressive resident rates. You may file for tax reliefs.

What is taxable?

All income earned in the city-state are subject to tax. This includes ‘accrued in’ the city-state and those that are also received from outside the country. For tax purposes, all profits gained from any business or trade, those earned from investments (like dividends, rental, and interest), royalties and profits from properties are all subject to taxes.

For income received abroad, profits are considered to be taxable under the following terms from Section 10 (25) of the Income Tax Act:

a) if the profit is remitted, brought, or transmitted into Singapore.

b) if the profit is used to pay debts gained through trade or business carried in Singapore.

c) if the profit is used as payment for any moveable property purchased in Singapore (materials or equipment used to a taxpayer’s business).

Note that these terms will only be applicable to foreign income received in Singapore if said income is gained by any individual who is considered a resident of the city-state. In order not to discourage foreign investors from starting a business in Singapore and using its banking and fund management facilities, non-resident individuals who are not operating inside or from Singapore can remit their income while being exempted from taxation.

Moreover, foreign income from overseas investments are not considered within Singapore’s jurisdiction and therefore will not be taxable. This is part of the government’s efforts to promote the republic’s regionalisation efforts.

All individuals who are subject to foreign-sourced income will also be liable to tax reliefs and other credits offered under Section 50, 50A, or 50B of the income Tax Act.

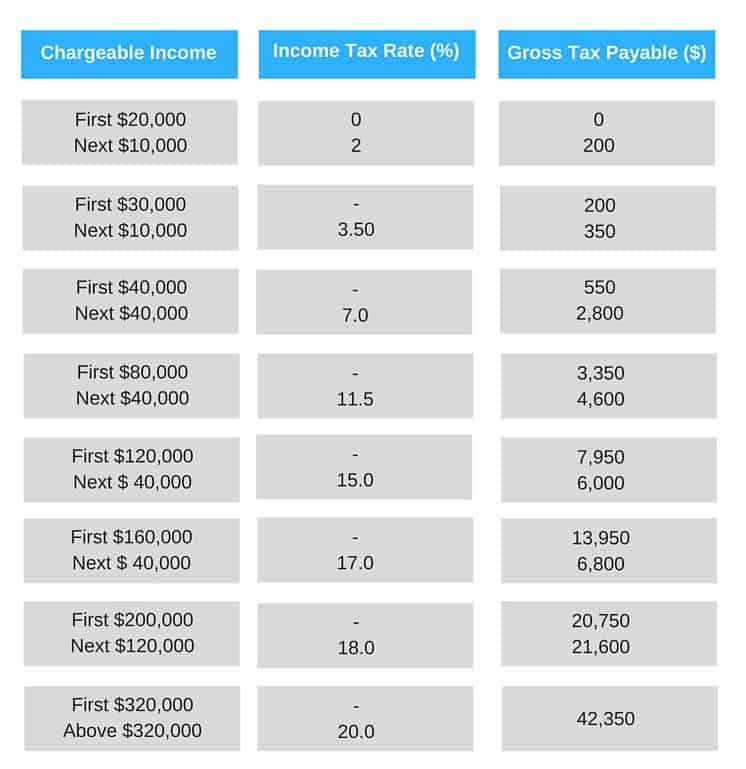

In Focus: Singapore’s Income Tax Rates for Residents

Singapore’s residents are charged with graduated rates that range from 0 to 20 percent. Check the table below for the income tax rate for specific salary brackets.

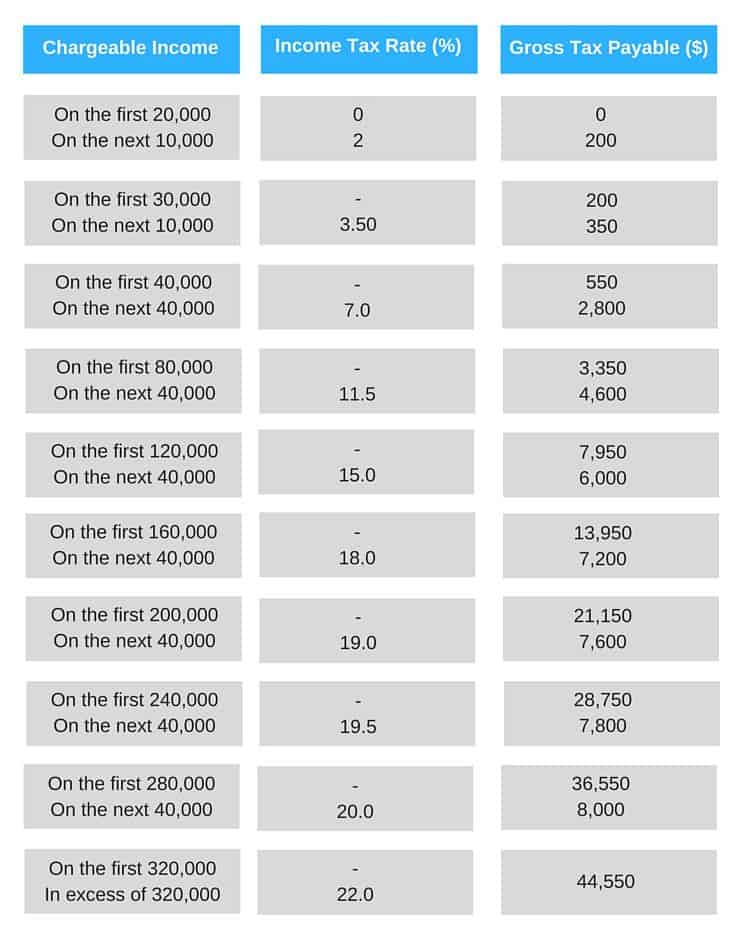

In 2017, Singapore is set to increase its taxes for those in the higher income bracket. Only those earning more than $160,000 a year will be affected by this hike. Below is the new table which will be effective come 2017.

Calculating personal taxes are again dependent on whether you are a resident or non-resident. You can click on this online calculator to estimate your annual individual income tax.

From Filing to Managing: How To Be Organised With Your Personal Income Taxes

Singapore may be known for its business-friendly laws, rich startup scene, and flexible immigration policy, but there is another aspect where it gets considerable credits is its comprehensive but simple method of filing taxes.

The city-state’s tax-filing system has been converted into the electronic process in 1992, a shift which made the administrative process more efficient. Making the standard taxation procedures automated made the system less dependent to individual tax officers (whose expertise can be subjective), reducing the risk of corruption.

Types of Filing for Personal Income Taxes

There are three ways in which residents can file for their taxes. A description of each can be found below:

a) E-Filing

To be liable for e-filing, personal taxpayers need to get a SingPass or IRAS Pin that they can use to access the e-service. The SingPass password is the most convenient one because it can be used to other government e-services and can be applied for online. The IRAS pin, on the other hand, is sent to the individual after 4 working days from online enrollment.

The SingPass or IRAS Pin can be used to log in to myTax Portal. Note that the online portal requires a number of documents including the Form IR8A (if your employer is not a part of the Auto-Inclusion Scheme), documents for the particulars of your dependents (e.g. parents, children), rental income from properties and other income if applicable, and Partnership Tax Reference Number/Business Registration Number for self-employed individuals.

The myTax Portal will require the individual to indicate all his or her income, deductions and reliefs received from organisations under the Auto-Inclusion scheme, reliefs claimed during the previous year, as well as tenanted proper information declared during the preceding year or as indicated on your e-Stamping records.

The online portal will also ask for the updating of any existing tax reliefs in the event that a taxpayer no longer qualifies for one, or for the amendment of the other amount of reliefs shared with other claimants. Moreover, other sources of income should be declared here if the individual has received other sources of income that are not pre-filled. Once successful, an acknowledgement page will be provided to the taxpayer as proof of a successful transaction.

b) Paper Filing

Under paper filing, the taxpayer is not required to declare his/her employment income received from an employer participating in the Auto-Inclusion Scheme. Paper filing already automatically includes this part in the income tax assessment. Instead, the taxpayer should indicate “0” for his/her donations and employment income as well as Central Provident Fund contributions and insurance premiums taken from their salary.

The filing resident individual should receive the following documents from the IRAS:

- Form B1 2016

- Appendices 1 and 2

- Guide to Completing Form B1

- Return Envelope

Under the NFS, individuals are not required to file tax returns. A Notice of Assessment (NOA) will be sent to the taxpayer which will include the auto-included income of the previous year’s relief claims. The responsibility of ensuring that the NOA is accurate is the responsibility of the taxpayer. If there are incorrect data, report it to the IRAS within 30 days from the date of issue of the NOA. Residents can check if they are eligible for NFS in MyTax Portal.

Payment Options

Residents can pay their personal taxes through a number of options. Learn about each below:

a) GIRO

Many taxpayers prefer using this online application when paying their taxes. Not only is it cashless, electronic, and timely, the app also offers interest-free installments of up to 12 months or annual deductions. Tax refunds are also received faster and are directly credited to the bank account of the taxpayer so that misplaced checks are no longer a concern.

b) Internet Banking

For internet banking, individuals need to log in to the banking portal of their respective bank, select the option “Bill Payment” and indicate IRAS as the billing organization. Put in the Payment Slip No. or Tax Reference No. and indicate the amount to pay (note that the amount is subject to the daily payment limit of the bank). A payment slip will then be issued together with the tax bill. Payments are posted three working days after the payment is done.

c) Cash/NETS

Taxpayers can make payments by cash, NETS, or cheques at any Singapore Post Branch. A payment slip is needed to make the payment and a receipt will be issued after a successful transaction. The payment will be posted on the account after three working days.

d) Cheque/Cashier’s Order

This mode of payment can be transacted at any bank in Singapore. Note that no receipt will be provided for this payment. However, in order for your payment to be credited properly, you need to make sure to attach the lower portion of your Payment Slip to the cashier or cheque order. For those who do not have a Payment slip, the Tax Type, and Tax/Document Reference No. need to be indicated at the back of cheque/cashier’s order. For other required details, check out this page.

e) Telegraphic Transfer

This option is best for those who are currently not in Singapore but have an overseas bank account. To use the Telegraphic Transfer, call the IRAS to get the Bank Account number and indicate your name, tax reference no., taxpayer’s name (if different), and purpose of payment (e.g. Tax Clearance, Individual Income Tax, S45 Withholding Tax). Taxpayers have to indicate that other agent bank charges are to be shouldered by the applicant instead of the beneficiary. When making the remittance, the amount paid should already include the bank charges required by the overseas bank as well as the intermediary bank in Singapore.

Managing Your Taxes

To properly manage your tax payments, you can check the myTax Portal to get the electronic copy of your bill or see if your payment has been properly filed by the IRAS. Taxpayers can also access the IRAS hotline at 800-356 8300 (or +65-6356 8300 for overseas) for other concerns.

Personal Income Tax: Everything Non-Residents Should Know

Who are considered as non-residents in Singapore jurisdiction? There are two terms that define this type of residency.

- Individuals who have worked in Singapore for 61 to 182 days.

- Individuals who worked for 60 days or less. Short-term employments are exempted from taxes. However, it does not apply if the individual is a professional, a director, or a public entertainer. Absences from Singapore that are part of the employment requirements are also not counted. In this case, the individual’s total income and the profit he/she earned outside of Singapore is fully taxable.

Which aspects of non-residents’ income are taxable?

a) Director’s Remuneration

There are three scenarios that can fall under this specific category. Remunerations received by the director as a member of the board regardless of whether the individual is physically in Singapore during the remuneration, gains from Vesting of Stock Awards (ESOW) or from Exercise of Stock Options (ESOP), and remunerations gained as an executive director and board director. The 22% non-resident individual tax rate will apply under these conditions.

b) Non-resident professionals

The tax rate of15% will apply to the gross income/fee derived by non-resident professionals gained though cash and non-cash payment of reimbursements for accommodation, airfare, allowance, transport, honorarium/speaker’s fee, and per diem.

c) Public entertainers

This category includes musicians, athletes, artists, and individuals with similar professions. A 10% concessionary rate will be charged to the total amount of income gained from the services that were performed in the city-state. This rate was reduced from the original 15% and will be considered official until March 2020.

d) Foreign property owners

A rate of 22% will be taxed from income gained from the rental and sale of properties of foreign owners.

e) Interest and royalties

For interest and royalties, a withholding tax rate of 10% will be imposed on interests, commissions, and other payment done in connection with any loan as well as lump sum payments and royalty of moveable properties.

Non-resident Income Tax Rates: A Summary

For non-residents, a flat tax rate of 15% or the progressive resident tax rates, whichever is higher, is charged from their profits. Consultation fees and Director’s fees are charged a higher amount, however, at a rate of 20%.

Come 2017, the taxation for non-residents (except those who have reduced final withholding tax rates) will be increased to 22%. The change is decided upon by the government to keep the parity between the taxes of the non-residents and the top marginal rates of the residents.

To calculate your income tax, use this online calculator.

Managing Your Income Taxes as a Non-Resident

Non-residents need to file Form M which can be requested from the IRAS. This form is only available in hardcopy so it is highly suggested to contact the tax-managing body if it isn’t received between February and March of every year.

For payment options, non-residents can pay their taxes using the same channels available for residents.

Deducting the Numbers: How To Make Your Taxes More Friendly To Your Pocket

Tax deductions, similar to withholding tax rates, differ according to the residency of an individual. Residents are entitled to claim donations, tax reliefs, and expenses, for example, to lessen the deductions to their total income. The total profit with all the tax reliefs subtracted is going to be the final amount taxed by the progressive rate.

Below is a list of Tax Reliefs for Resident Tax Payers

a) Employee Deduction

Employees can claim deductions for expenses they spent from their personal income for things necessary for their employment. This can include travel costs, subscriptions, entertainment expenses, etc.

b) Costs Incurred by Sole Proprietors, Self-employed individuals, or Partners

This category, which includes freelancers, taxi drivers, commission agents, etc., can claim tax deductions for the following:

- Business expenses

- Capital Expenditure incurred on renovation or refurbishment

- Productivity and Innovation Credit

- Capital Allowances on fixed assets

- R&D Expenditure

- Medical Expenses

- Land Intensification Allowance

- Unabsorbed capital allowances and Business making losses

- Expenses incurred before start of business

c) Rental Expenses Deductions

Residents can claim this given that the expense is incurred only for the use of producing rental income and made during the tenancy period.

d) Donations Deductions

Taxpayers can claim deductions of 2.5 to 3 times the amount of cash, shares, computer, artefact, land and building donations, and public art incentive schemes (incurred from 2009 to 2018).

e) Angel Investors Tax Deduction Scheme

Residents are liable to tax deductions when they have invested in qualifying start-up companies, invest at least $100,000 within 12 months from the date of first investment in the same company, and maintain an investment for a continuous period of 2 years. You can check out this page for more detailed information.

f) Rebates and reliefs

Tax residents are entitled to a number of reliefs and rebates given that they meet certain qualifying conditions. These tax reliefs and rebates (which includes Supplementary Retirement Relief, Handicapped Parent Relief, and Earned Income Relief to name a few) are designed to promote specific economic and social objectives. A full list of these can be found here.

g) Personal Income Tax Relief Cap

Starting 2018, the total of personal income tax reliefs that residents can apply for will be subject to a relief cap of $80,000 per Year of Assessment. Reliefs exceeding this cap will still be imposed a limit of $80,000.

Note that non-residents are liable to claiming donations and expenses. However, they are not entitled to rebates and tax reliefs.

Singapore’s Taxation System

With its economic goals, Singapore was able to procure a taxation system that, while complicated in some aspects, is definitely friendly to taxpayers—residents or not. Hiring a professional accounting and tax provider can be a good workaround this system, especially for company directors and others who want to focus on their business.

The advantage of the city-state’s set of rules is that it still adheres to its business aims, as seen from its efforts of exempting certain individuals to avoid them from being discouraged to work in the Republic. This even influences taxation rules for startups, which is further proof that the city-state has a solid set of vision for its economy.

Need tax assistance?

We ensure the accurate and timely filing of our clients’ taxes. Avoid late submissions and penalties by letting our tax team assist you!

Contact Us Now